Federal Budget 2026: Property, negative gearing and capital gains explained

With all the noise around the Federal Budget, we wanted to cut through it and give you a clear, factual summary of the proposed changes to negative gearing and capital gains tax and what they actually mean for you.

One important note before we get into the details: these are tax-related changes, not a property strategy in themselves. They are a consideration to factor into your decisions, alongside everything else that drives a sound long-term plan.

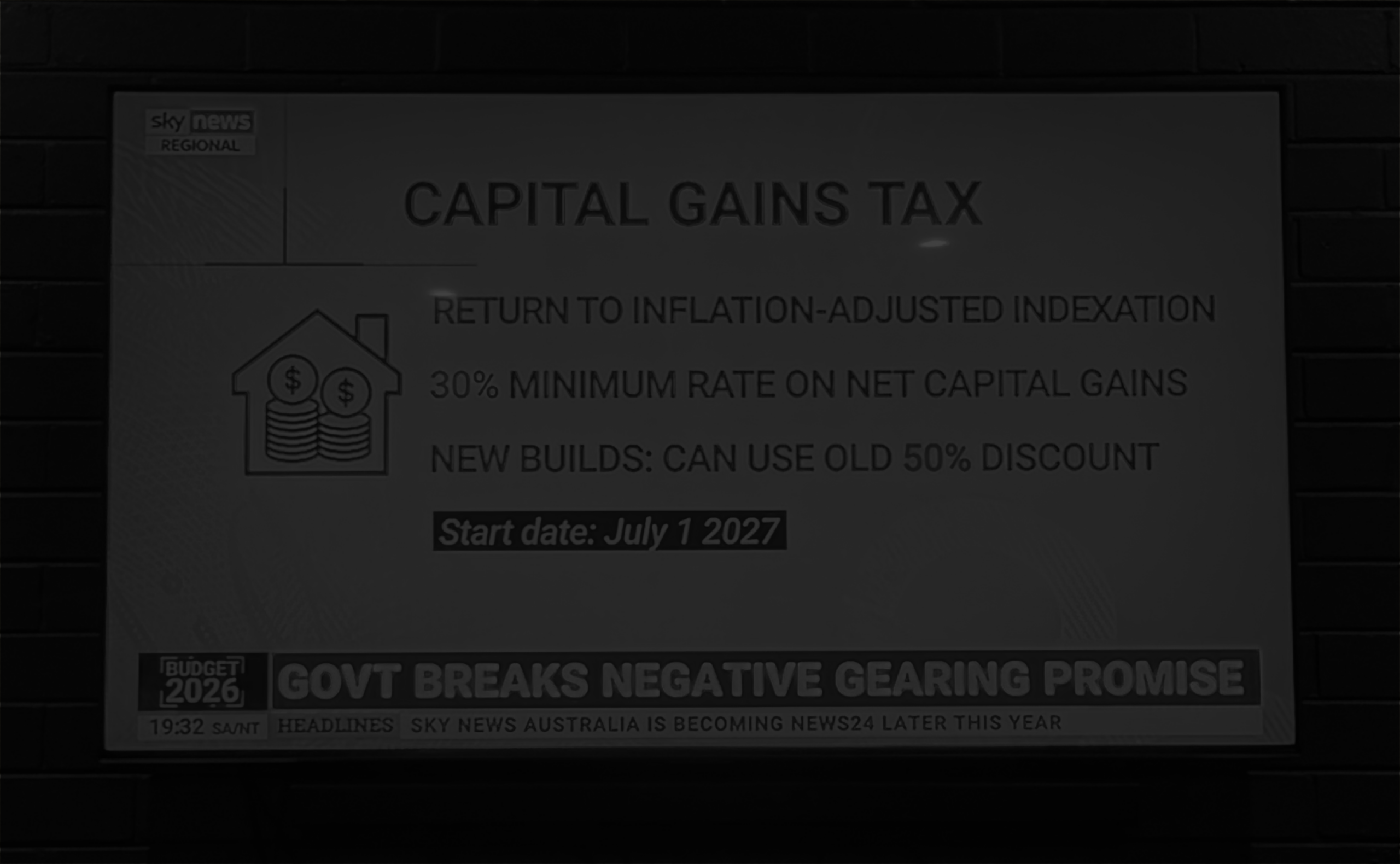

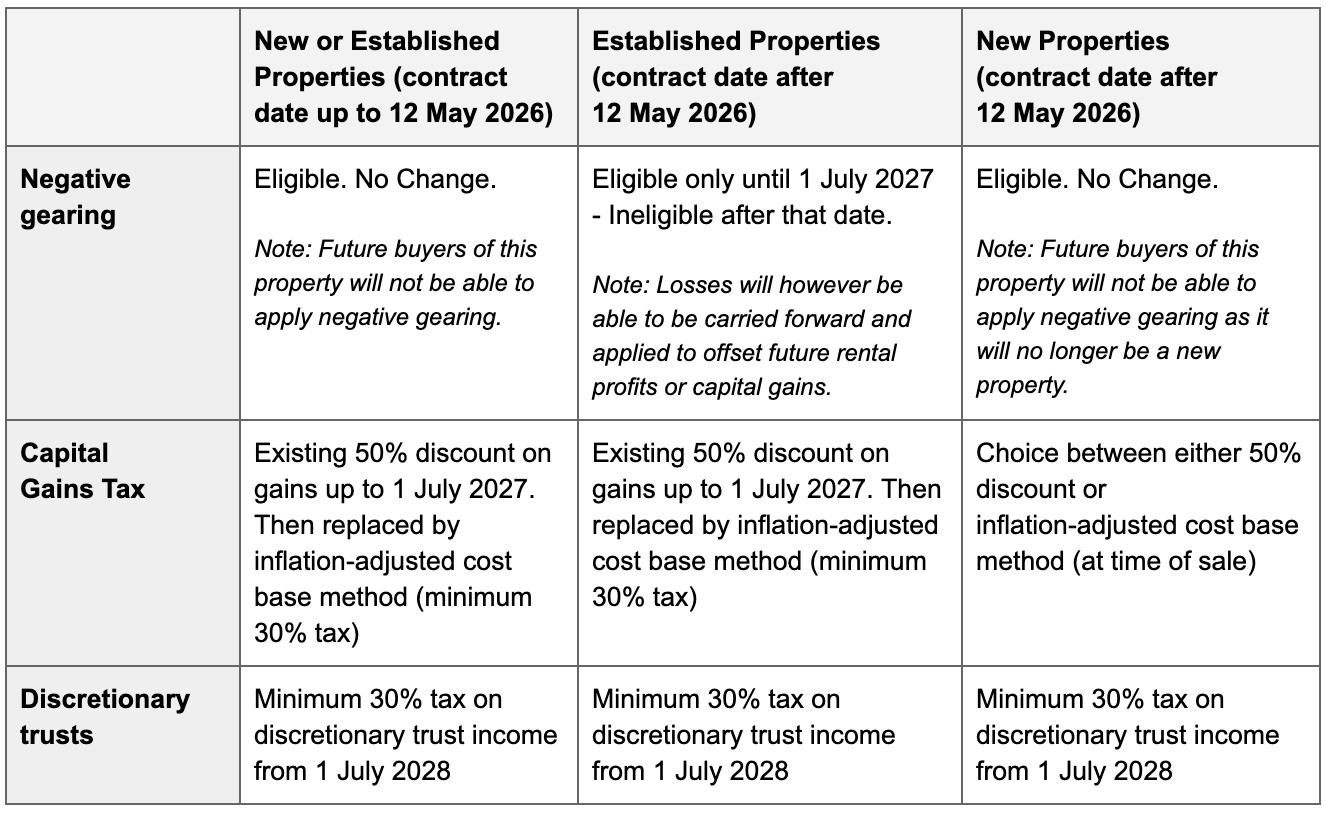

The proposed changes at a glance

What the government itself is forecasting

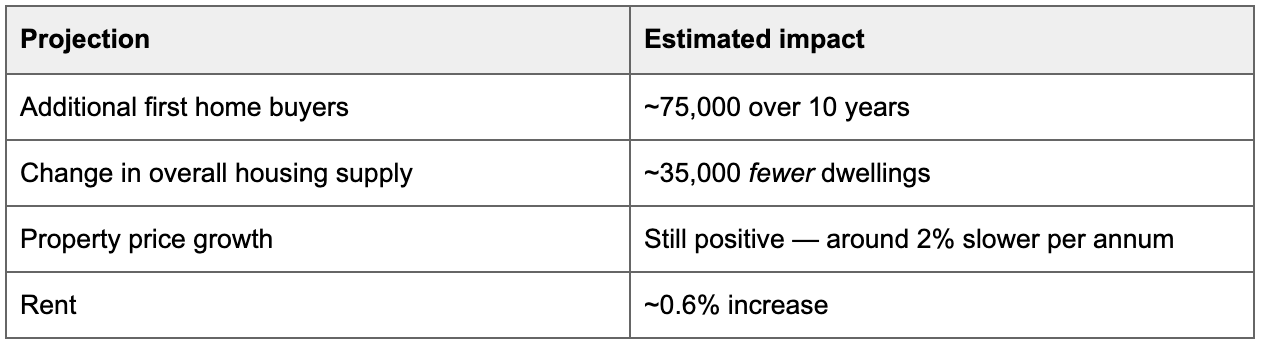

For context, here is what the government’s own modelling projects over the next decade:

Less supply and only marginally slower growth tells its own story. We’ll let the numbers speak for themselves.

What this means by scenario

If you already own an investment property

Your negative gearing arrangement is fully grandfathered, nothing changes there.

On CGT, any gains accrued up to 1 July 2027 continue to attract the 50% CGT discount. From 1 July 2027 onwards, any further gains on the property will be taxed under the new inflation indexation method with the 30% minimum. You will have the choice to split these gains using either a time apportionment method (% of years owned pre vs post 1 July 2027) or by obtaining an official market valuation at 1 July 2027

If you are looking to buy an established investment property

From 1 July 2027, Established properties purchased after 12 May 2026 will be ineligible for negative gearing income tax offsets, losses however will be able to be carried forward, and used to offset future ongoing rental profits and/or capital gains from its sale.

If you are considering a new build

New builds are exempt from the negative gearing changes, and at time of sale, investors will have the choice between the existing 50% CGT discount or the new inflation-adjusted cost base method.

It is too early for us to interpret exactly what this could mean for the new-build market, we are working through the details and will share considered analysis once the picture is clearer.

If you are a home owner

Last night’s changes do not directly affect your home. The principal place of residence exemption is intact, when you sell your home you continue to pay zero CGT. Negative gearing does not apply to your own home either.

If you hold property in a discretionary trust, please note a new minimum 30% tax on discretionary trust income comes in from 1 July 2028. If that could apply to you, it is worth a conversation with your accountant well ahead of time.

Our view

These are meaningful changes, but they are not the crisis some headlines will suggest. Property has absorbed policy shifts, rate cycles and economic uncertainty for decades. The fundamentals of well-chosen property in the right locations have not changed overnight.

What has changed is the importance of understanding how these tax considerations fit into your individual situation, particularly before 1 July 2027.

We are working through what these changes mean and are very happy to talk through your specific position, whether you are an existing investor, actively looking, a home owner, or simply weighing your options. Feel free to simply reply to this email or book a time to chat with me directly here.

Get in touch